SPRING CHECK-UP

Dear Clients and Friends,

For this edition of The Novack Team Update we’ll be taking a closer look at the state of the market and its underlying drivers…

1Q19 Market Overview

- While the overall Manhattan absorption rate is 7 months, properties priced above $2 million have supply levels >10 months, and those priced above $6 million have more than a 1-year supply. (The historic range of equilibrium for the New York City market area is 6-9 months.) The sustained excess inventory at the top end signifies that this segment continues to necessitate price reductions from sellers.

- After a prolonged lack of consensus between buyers and sellers, we are now witnessing many sellers discount their properties to current market conditions:

- 1Q19 data reflected an overall ~9% price discount, with sales between $1 and $10 million averaging approximately 11%, and discounts well above 20% for properties greater than $20 million.

- We are consequently starting to see more buyers willing to transact as they perceive value in the market. Contracts signed for 1Q19 increased 4% year-over-year.

New Development Overview

- There is a surplus of in-place and to-be-listed new development product which, according to many estimates, could take approximately 5 years to be fully absorbed at the current sales pace.

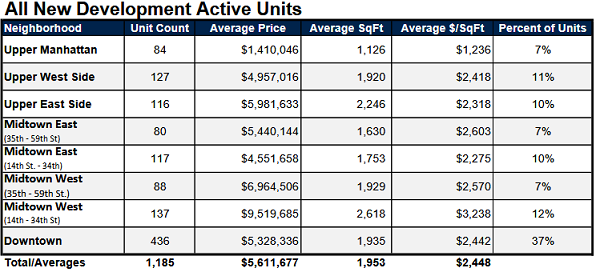

- The above fact underscores downward pressure on pricing. When one looks more closely at Manhattan actively listed units, however, there is a finite number of properties available in prime neighborhoods, and they carry a relatively high average price/SF of $2,448. (*Table below based on third-party May 1st Data.)

- New developments actually encompass a relatively limited portion of the overall Manhattan residential market — representing only ~8% of total co-op and condo inventory. Accordingly, they may not be as relevant to many buyers depending on their square footage/location/budget parameters.

- For those who are focused on new development listings, there are certain opportunities to purchase at discounts to asking due to:

- Oversupply and relatively high price points.

- Some sponsors facing time-sensitive pressure to close deals in order to pay down construction loans with looming maturity dates and frequently limited opportunity to refinance, given current achievable sale pricing vs. when loans were originated in stronger markets.

- Unless the price of developable land in NYC decreases there should be a tempering of new construction projects originated in the near term due to the thin margin between project costs and achievable sale execution. A lessening of new supply, and gradual absorption of in-place units, should eventually lead to greater equilibrium.

Mortgage Rates

Mortgage rates are still historically low and expected to remain so for the balance of 2019. Locking in attractive long-term financing presents an appealing prospect for buyers.

Mansion and Transfer Tax Changes

The increase in mansion and transfer taxes will take go into effect on July 1, 2019.

- State Transfer Tax: currently 0.4%, will increase to 0.65% for residential sales above $3 million.

- Mansion Tax: currently 1% and will be amended as follows:

- From $2,000,000 to less than $3,000,000: 1.25%

- From $3,000,000 to less than $5,000,000: 1.5%

- From $5,000,000 to less than $10,000,000: 2.25%

- From $10,000,000 to less than $15,000,000: 3.25%

- From $15,000,000 to less than $20,000,000: 3.5%

- From $20,000,000 to less than $25,000,000: 3.75%

- $25,000,000 and greater: 3.9%

The above tax changes may have some dampening effect on the market (particularly at the very high end and in the short term) but ultimately will probably not be as impactful as the other considerations above.

Please don’t hesitate to reach out to us with any questions, or on any of your real estate needs.

Warm Regards,

Alex and Sybille